Disrupted: Challengers Finally Overtake Incumbents

The global pandemic brought on by COVID-19 has fundamentally changed consumer behavior and transformed the Commerce Continuum, where the accelerated adoption of digital capabilities and e-commerce has entirely reshaped retail, payments and banking in less than 12 months. The data points are telling: Square estimates that the decline in cash usage in the past twelve months would have taken three years without the pandemic¹. At the same time, e-commerce grew by more than 40%, banks saw digital sales increase from 25% pre-COVID to 75% during COVID and the use of FinTech apps increased more than 70% through the pandemic².

This digital acceleration created an imperative for incumbents to provide virtual-only experiences powered by a new class of enablers that can be more easily implemented than those offered by legacy providers. Banks that historically took a long time to test, negotiate and implement new capabilities are now moving at lightning speed to deploy new infrastructure and products. Retailers that were reluctant to update their tech at all are rushing to implement a more modern-commerce stack and enable new shopping experiences in their stores. Payment companies saw such a large increase in e-commerce volume that it neutralized the sudden decline in physical retail sales.

Alongside this new tech imperative, digital acceleration has also led to a shift in the balance of power between incumbents and challengers. Category leaders across commerce that have been historically unrivaled in size and influence did not just see an assault on their dominance…they were overtaken. In many cases, it happened decisively and with valuations that reset expectations for the entire industry. COVID-19 did not just accelerate digital adoption, it triggered a seismic shift in the market and compressed a decade of change into a year. As a result, well equipped challengers were able to surpass their incumbent rivals.

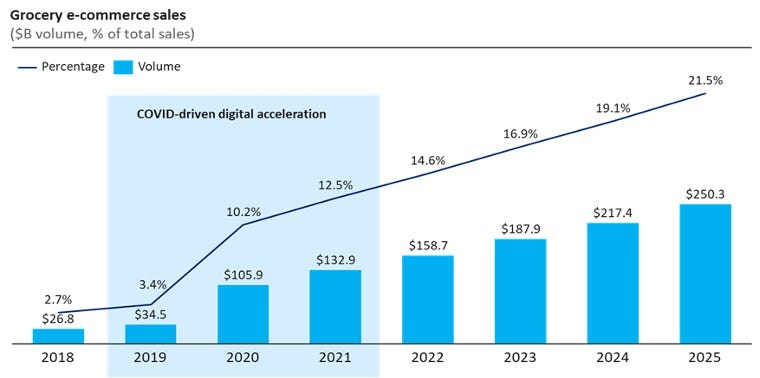

In retail, COVID dramatically amplified consumer preferences for grocery delivery. Nowhere was this shift more pronounced than in the growth of Instacart, where the company delivered more food in the first two months of the pandemic than Walmart, Kroger or Albertsons. The company grew 300% year-on-year and hit $1.5B in revenue³. At the same time, it’s valuation doubled twice in less than 12 months — with a $200M round valued at $18B in October 2020 and a $265M round valued at $39B in March 2021⁴.

Today, the valuation of Instacart has surpassed the market capitalization of both Kroger ($27.7B) and Albertsons ($8.7B). Not only has Instacart overtaken the largest grocers, but it has redefined the business model for grocery. More than 600 retailers across 45,000 locations have commercial relationships with Instacart⁵. These retailers pay Instacart 10% of the order value, unable to effectively (or profitably) provide delivery services on their own. A company less than 10 years old displaced Kroger — nearly 150 years old — and in the process disrupted the grocery category forever.

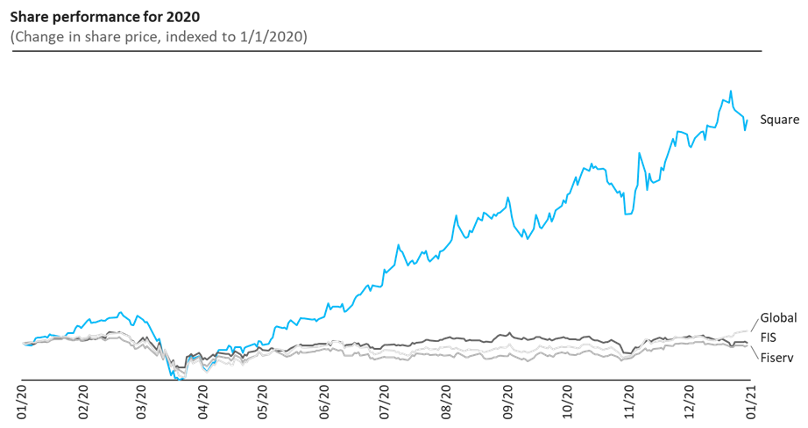

In payments, the toppling of incumbents has been even more dramatic. Square’s revenue doubled between 2019 and 2020, while its gross profit increased by nearly 50%⁶. A lot of this growth was driven by a 50% year-on-year increase in the total number of active Cash App users (36M v. 24M)⁷. On average, these users made more than 15 transactions per month across spending, saving and investing. Overall, the growth in consumer payment usage accounted for 45% of total gross profit, up from 25% in 2019⁸.

Square’s total growth has been driven by this two-pronged strategy: grow consumer usage of its financial products while driving continued market and product expansion into the seller (e.g., merchant) segment. The impact of this strategy is self-evident. The company grew 102% between 2019 and 2020, compared to an average 39% for the largest existing incumbents⁹. At the same time, its enterprise value increased to $97B — surpassing valuations of the largest incumbent payment processors (FIS = $106B, Fiserv = $96B, Global = $72B)¹⁰ .

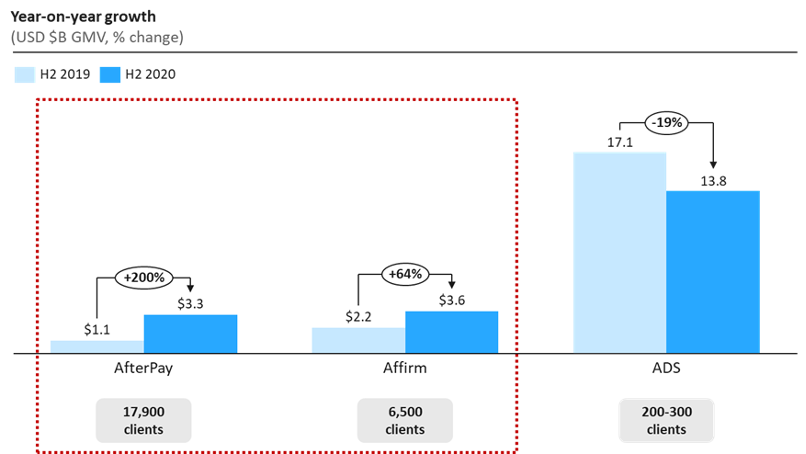

Square is not the only entity that has reset expectations and surpassed the largest existing financial services incumbents. The ascendency of Klarna, Affirm and AfterPay have fundamentally transformed legacy point-of-sale finance and reimagined the category as Buy Now Pay Later. Benefitting from the secular acceleration of e-commerce and consumer preferences for credit alternatives, these players have seen dramatic expansion in revenue and user growth — at the same time as incumbents have faced meaningful headwinds.

Together, Klarna, AfterPay and Affirm have close to 17M active consumer accounts and nearly 30,000 merchants in the United States¹¹. This dwarfs the scale of legacy private label providers — including Synchrony and Alliance Data. Reflecting investor belief in the ability to drive category disruption, the valuation of these players has surpassed legacy entities: Klarna at $31B, Affirm at $21B and AfterPay at $23B versus Synchrony at $27B and Alliance Data at $11B¹².

While disruption in Buy Now Pay Later has been developing across several players for the past few years, disruption in retail trading has happened more suddenly. A sector, long dominated by traditional heavyweights like Schwab, has been fundamentally challenged by the rapid ascendancy of Robinhood. This ascendency was accelerated through COVID. The pandemic led to tens of millions of lost jobs. It also led to the most dramatic increase in consumer savings of the last decade. This asymmetry — alongside the boredom of shelter-in-place restrictions — led retail investors to jump into the stock market at historic levels.

The resulting numbers are staggering. In June 2020, Robinhood’s daily average volume levels outperformed all publicly traded trading platforms¹³. Its user base is estimated to have doubled in the past twelve months, with more than 20 million registered accounts on the platform today¹⁴. This growth has accelerated in the past quarter, tripling the number of daily unique users and increasing site traffic by more than 1,200% for the week of January 25.¹⁵

At the same time, the average investor on Robinhood looks very different from other trading platforms — with the average account holding $5,000 compared with $240,000 at Schwab and $110,000 at TD Ameritrade¹⁶. This mass popularization of trading is arguably the single most important disruption posed by Robinhood and caused it to become a lightning rod in a public discourse around the democratization of wealth. It equips and empowers individuals, that have historically sat on the sidelines of investing, to enter the market through micro trades — delivered via a user experience that is more akin to a challenger bank than a Bloomberg terminal.

Robinhood’s growth transformed the industry in less than 12 months. It has confidentially filed for an IPO and bids in the secondary markets place its valuation north of $40B. Its ascendency triggered a forceful response by incumbent players — the consolidation of the largest independent trading platforms through two deals that closed in October 2020. The first deal was the acquisition of E*TRADE by Morgan Stanley for $13B and the second was the acquisition of TD Ameritrade by Schwab for $22B. Both deals were designed to bolster a defense against the most significant disruption in retail trading since the creation of E*TRADE in 1982.

What does all of this mean for us? First, now more than ever, incumbents need to invest in digital capabilities to compete with challengers. Our conversations with dozens of large incumbents suggest a recognition of this imperative and an increase in tech investment over the next 12 months. Second, challengers will continue to look for best-in-class tech to support their products and services.

We see the impact of these two implications across our portfolio. Several companies power Instacart’s tech stack. Square, Affirm and AfterPay are working with companies like Marqeta to enable digital card experiences. At the same time, incumbents like FIS and Fiserv have acquired, as well as partnered with, other portfolio companies — including Radius8, MX, Forter and Socure. Beyond these examples, the digital acceleration coming out of COVID has led to revenue growth across many of our portfolio companies.

While the market is still in a moment of uncertainty, we believe that this acceleration thesis is a lasting outcome from the pandemic. As one executive at Shopify noted, “COVID has acted like a time machine; it brought 2030 to 2020” ¹⁷. This back-to-the-future of commerce will impact incumbents and challengers alike. The rules, expectations and models of a pre-COVID market have shifted and investment in tech is an even greater requirement to compete. We already see the impact in the market. Grocers that have not meaningfully innovated in decades are now dedicating hundreds of millions of investment for new digital capabilities. Banks are actively looking to double-down on tech partnerships and digital capabilities. As we look to the year ahead, we believe that our core focus on enablers will continue to benefit from the tailwinds of these secular trends — and position our overall portfolio for continued growth.

[1] Company filings.

[2] Morgan Stanley: Did the Pandemic Change E-commerce Forever? February 26, 2021. CNBC interview with PNC CEO on May 14, 2020. EY: How COVID-19 has sped up digitization for the banking sector. November 3, 2020.

[3] Forbes: Instacart Survived COVID Chaos — But Can It Keep Delivering After The Pandemic? January 27, 2021.

[4] CNBC: Instacart’s Valuation Doubles to $39 Billion. March 2, 2021.

[5] Forbes: Instacart Survived COVID Chaos — But Can It Keep Delivering After The Pandemic? January 27, 2021.

[6] Company filings.

[7] Ibid.

[8] Ibid.

[9] Annual and quarterly filings for Square, Fiserv, FIS and Global Payments.

[10] Yahoo Finance (all valuations as of 12/31/2020).

[11] Company filings.

[12] Yahoo Finance.

[13] Bloomberg: Robinhood Blows Past Rivals in Record Retail Trading Year. August 10, 2020.

[14] Morningstar: Robinhood: What to know before it goes public. March 23, 2021.

[15] Seeking Alpha: Robinhood trading volume keeps snowballing, even amid controversy. February 8, 2021.

[16] Morningstar: Robinhood: What to know before it goes public. March 23, 2021.

[17] Wall Street Journal: COVID-19 Propelled Businesses into the Future. Ready or Not. December 26, 2020.